Expected Sector Development

The market research institute Drewry expects global container throughput to rise to 2.1 % in 2017 following weak growth in 2016 and the previous year. Momentum should come from the South Asia (+ 5.9 %), Central America (+ 4.0 %) and the US East Coast (+ 3.7 %) shipping regions in particular. Throughput growth of 2.4 % is forecast for China, the Port of Hamburg’s most important shipping region. This represents a recovery of 0.5 percentage points after a significant downturn in 2016. Drewry expects slower growth of 1.6 % for the European ports in the forecast period. However, trends in the individual shipping regions will be mixed. Whereas Drewry’s experts anticipate weaker throughput for the shipping regions of North-West Europe, the Eastern Mediterranean and the Black Sea, growth rates in Scandinavia and the Baltic region are expected to more than double. This could have a positive impact on transshipment volumes at the North Range ports, although some cargo will find its way to the Baltic Sea via direct routes.

in % |

2017 |

Trend vs. 2016 |

||||

|

||||||

World |

2.1 |

|

||||

Europe as a whole |

1.6 |

|

||||

North-West Europe |

1.2 |

|

||||

Scandinavia and the Baltic region |

3.2 |

|

||||

Western Mediterranean |

2.1 |

|

||||

Eastern Mediterranean and the Black Sea |

1.4 |

|

||||

However, in light of the subdued volume trend as a whole and existing terminal capacities in the North Range and Baltic Sea, competition between the ports is likely to remain fierce in 2017. The container shipping market will continue to see a structural surplus of ship space in 2017. According to estimates of market research institute Alphaliner, growth in total capacity of the container ship fleet will slow as a result of declining orders from shipping companies and delayed deliveries. However, at 3.4 %, growth in total capacity of the container shipping fleet will outpace global container volumes at the ports in the forecast period.

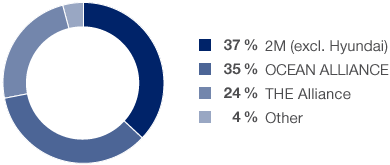

Capacity Breakdown by Shipping Line Alliances Following Reorganisation

on Far East–Europe Services as of 31 December 2016

Source: own presentation, Alphaliner Monthly Monitor, January 2017

In order to stabilise the market amid this growing capacity surplus, the sector has been dominated by acquisitions and mergers as well as the formation of new alliances since 2015. After the world’s two largest shipping companies – Maersk and MSC – launched joint operations as the 2M alliance in early 2015, two further newly formed alliances will begin operating in April 2017: Cosco, Evergreen, OOCL and CMA CGM will pool their services on the east–west trades under the name “OCEAN ALLIANCE”. Hapag-Lloyd/UASC, K-Line, NYK, Yang Ming and MOL are combining their services as “THE Alliance”. Maersk announced that Hamburg Süd will continue to operate as an independent brand following the planned takeover. However, exact details of the integration are not yet known. The takeover is currently being examined by the competition authorities. The ongoing concentration process and the formation of new consortia will lead to the pooling of container services and timetable changes.

Despite the modest container throughput forecast for the north-western European ports, stable or rising transport volumes are expected for pre- and onward-carriage systems in hinterland traffic. Based on the throughput forecasts, hinterland traffic between the Northern Adriatic seaports and south-eastern Europe is also likely to increase. In light of the ongoing increase in ship sizes and the associated increase in container volumes per ship call, the pressure on terminals and hinterland transport systems will continue to rise.

According to the most recent medium-term forecast on cargo and passenger transport issued by the German Federal Ministry of Transport and Digital Infrastructure (BMVI) in summer 2016, transport volumes are expected to increase by 0.3 % and traffic performance (transport volume multiplied by the distance travelled) by 1.6 % in 2017.

The North European coast. In the broadest geographic sense, this is where all the international ports in Northern Europe from Le Havre to Hamburg can be found. The four largest ports are Hamburg, Bremerhaven, Rotterdam and Antwerp.

In maritime logistics, a terminal is a facility where freight transported by various modes of transport is handled.

A port’s catchment area.