Market Position

With its listed core business Port Logistics, HHLA operates on the European market for sea freight services. This market offers long-term growth prospects as a number of key Central European countries strengthened their competitiveness after the debt crisis, thereby paving the way for a further increase in foreign trade and consumer spending. Eastern Europe also offers growth potential and stable forecasts. Whether these positive trends materialise depends on the resolution of regional conflicts and the development of fuel and energy prices.

The relevant economic indicators suggest that the European Union can expect a steady increase in gross domestic product. Due to the persistently high debt rate, however, stronger growth is only expected in the medium and long term. In the short term, external factors and unresolved structural problems will impact containerised trade and transport volumes.

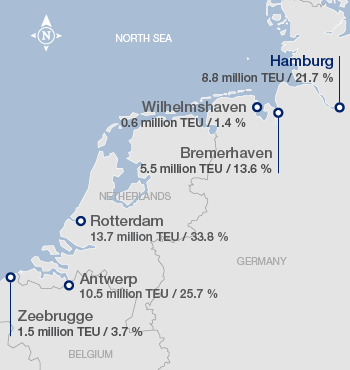

Throughput at the North Range Ports

Volumes and market shares, 2017

Source: Port Authorities / own calculation (market share)

The market for port services on the Northern European coast (the North Range) of relevance for HHLA is characterised by its high concentration of ports. Competition is particularly strong between the four major North Range ports of Hamburg, HHLA’s main hub, Bremerhaven, Rotterdam and Antwerp. Other handling sites – such as Wilhelmshaven and Zeebrugge – are considerably smaller in terms of their capacity and/or current freight volume. At present, the Baltic Sea ports are primarily served by feeder traffic operating via central distribution points in the North Range. The practice of ocean-going vessels calling directly at ports such as Gdansk or Gothenburg has also established itself, however, and is increasingly competing with this network system. Adriatic ports, such as Koper, and the Polish ports have also improved their infrastructure and are competing with the Port of Hamburg for freight in the hinterland.

As well as the geographical position and hinterland links of a port, its accessibility from the sea affects the competitive position of terminal operators. Local freight volume in the direct catchment area of each port location plays an important role. Other key competitive factors that influence market position include the reliability and speed of ship handling, the scope and quality of container handling services, as well as the performance of pre- and onward-carriage rail systems serving the hinterland (e.g. frequency, punctuality, pricing).

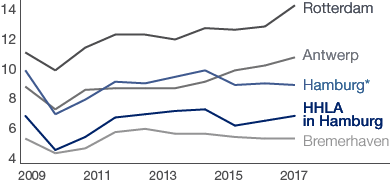

Container Throughput at the Largest North Range Ports

in million TEU

Source: Port Authorities; *incl. HHLA

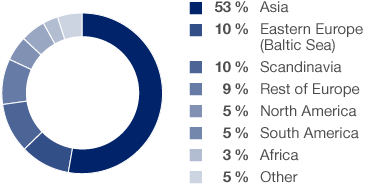

Seaborne Container Throughput by Shipping Region

in the Port of Hamburg, 2017

Source: Hamburg Hafen Marketing e.V.

Apart from a change in the ownership structure at the remaining terminal in Zeebrugge, there were no changes at the rival ports in 2017. Competition remains extremely fierce and the ports are increasingly dependent on changing shipping company constellations. The resulting shift towards more geographically flexible feeder traffic is having a significant impact on handling volumes. By contrast, the market position for handling volumes that are tied to the natural catchment area onshore is largely stable – given that it is vital to take the shortest route for the disproportionately more expensive land-bound transportation.

The Container segment benefits from the Port of Hamburg’s position as the most easterly North Sea port, which makes it the ideal hub for the entire Baltic region and for hinterland traffic to and from Central and Eastern Europe. Furthermore, the long-standing trading relationships between the Port of Hamburg and the Asian markets are advancing Hamburg’s role as an important European container hub. With a container throughput of 8.8 million TEU, Hamburg ranked 18th among the world’s ports in 2017 and is thus the third-largest European container port after Rotterdam and Antwerp.

In Hamburg, HHLA expanded its position as the largest container handling firm with a throughput volume of 6.9 million TEU in 2017. The HHLA container terminals significantly increased their market share for handling at the Port of Hamburg to approximately 78 % (previous year: 73 %). Asia, Eastern Europe and Scandinavia were the most important shipping regions.

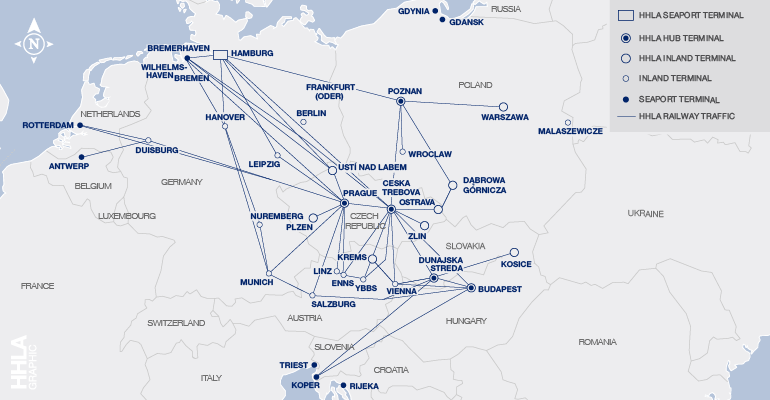

In the Intermodal segment, HHLA primarily utilises the advantages of the Port of Hamburg’s rail infrastructure – Europe’s most important rail traffic hub handling approximately 2.3 million TEU a year. HHLA’s Intermodal network also comprises further ports along the North Sea and Baltic Sea coasts as well as the northern Adriatic and, increasingly, continental traffic. The companies that transport containers by train compete with other rail operators and intermodal transport firms in Germany and abroad, but also with other carriers such as trucks and feeder ships. As the rail infrastructure is for the most part publicly owned, various national authorities guard against discrimination in both access and usage fees. In addition to the density of the available network, key competitive factors include the frequency of departures, opportunities for freight pooling and storage in the hinterland, the geographical distance to destinations, on-schedule operation and infrastructural capacity. The importance of these factors is growing as ports compete with one another.

Intermodal Network of HHLA

Selected connections

HHLA has proprietary inland terminals in Central and Eastern Europe along with its own container wagons and traction fleet (locomotives). All of these factors play a major role in the company’s service offer. This is necessary to enable it to run direct trains with frequent departures and to allow the efficient pooling of rail freight transported via the port, which is efficiently distributed by central handling facilities. HHLA occupies relevant market positions in the majority of the regions it serves. HHLA has a sound market position in the greater Hamburg metropolitan region in the delivery and collection of containers by truck.

The Logistics segment serves various market sectors, some of them heavily specialised. With its multi-function terminal, HHLA is the leading provider of specialist handling services in Hamburg. Via Hansaport, HHLA has a stake in Germany’s biggest seaport terminal for handling iron ore and coal. HHLA also provides fruit handling services for Northern Europe with its Frucht- und Kühl-Zentrum. In the field of consultancy, work is conducted on pioneering development projects around the world.

With a population of approximately 1.8 million and its significance as an economic centre, Hamburg is one of the largest property markets in Germany for the Real Estate segment. What makes the portfolio particularly attractive are its unique buildings and favourable locations in Hamburg’s Speicherstadt historical warehouse district and on the northern banks of the river Elbe/fish market area. The company has built up a wealth of development and implementation expertise dedicated to finding the right balance between market-based tenant demands and the careful handling of its landmarked buildings with world heritage status. The properties compete with German and international investors marketing high-quality properties in comparable locations.

The North European coast. In the broadest geographic sense, this is where all the international ports in Northern Europe from Le Havre to Hamburg can be found. The four largest ports are Hamburg, Bremerhaven, Rotterdam and Antwerp.

Vessels which carry smaller numbers of containers to ports. From Hamburg, feeders are primarily used to transport boxes to the Baltic region.

A port’s catchment area.

In maritime logistics, a terminal is a facility where freight transported by various modes of transport is handled.

A TEU is a 20-foot standard container, used as a unit for measuring container volumes. A 20-foot standard container is 6.06 metres long, 2.44 metres wide and 2.59 metres high.

A port’s catchment area.

A TEU is a 20-foot standard container, used as a unit for measuring container volumes. A 20-foot standard container is 6.06 metres long, 2.44 metres wide and 2.59 metres high.

Transportation via several modes of transport (water, rail, road) combining the specific advantages of the respective carriers.

In maritime logistics, a terminal is a facility where freight transported by various modes of transport is handled.

The action of a locomotive pulling a train.