Earnings Position

HHLA’s performance data developed positively in 2017. There was strong year-on-year growth in container throughput of 8.1 % to 7,196 thousand TEU (previous year: 6,658 thousand TEU). This rise resulted primarily from considerably higher volumes on the Asian trades and in feeder traffic with the Baltic ports. A further increase in transport volumes of 5.2 % to 1,480 thousand TEU was achieved (previous year: 1,408 thousand TEU). This trend was driven by growth in both rail and road transportation.

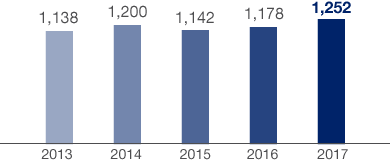

Revenue

in € million

Against this background, revenue of the HHLA Group rose by 6.3 % to € 1,251.8 million (previous year: € 1,177.7 million) in the reporting period. This was primarily due to volume-related growth in the Container and Intermodal segments. The listed Port Logistics subgroup largely developed in line with the HHLA Group as a whole. Its Container, Intermodal and Logistics segments recorded an overall increase in revenue of 6.5 % to € 1,220.3 million (previous year: € 1,146.0 million). The non-listed Real Estate subgroup succeeded in raising revenue slightly by 0.6 % to € 37.9 million (previous year: € 37.7 million). The Real Estate subgroup thus accounted for 2.5 % of Group revenue.

At € -0.3 million, changes in inventories once again had no material impact in the reporting period (previous year: € 0.3 million). Own work capitalised decreased to € 5.4 million (previous year: € 6.5 million).

The reduction in other operating income to € 39.4 million (previous year: € 57.5 million) was mainly attributable to the termination of the lease for the Übersee-Zentrum in the previous year.

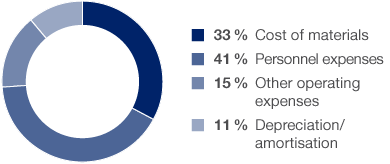

Operating Expenses

Expense structure 2017

The 4.2 % increase in operating expenses to € 1,123.2 million (previous year: € 1,077.9 million), meaning that all expenditure types than growth in revenue.

The year-on-year rise in cost of materials of 5.9 % to € 370.5 million (previous year: € 350.0 million). The cost of materials ratio remained virtually unchanged at 29.6 % (previous year: 29.7 %).

Personnel expenses rose by 4.7 % to € 463.8 million (previous year: € 443.0 million). In addition to higher union wage rates, the reasons for this rise included increased headcount in the Intermodal segment due to the expansion of business and greater use of external staff at the container terminals in Hamburg as a result of volume trends. Following restructuring-related expenses in the previous year – particularly in connection with the discontinuation of project and contract logistics – this year’s figure includes expenses for the organisational restructuring of the Container segment. The personnel expense ratio decreased to 37.1 % (previous year: 37.6 %).

Other operating expenses increased by 2.4 % in the reporting period to € 166.3 million (previous year: € 162.5 million). While the previous year’s figure included expenses for provisions in connection with an onerous lease in the Intermodal segment and the insolvency of the container shipping company Hanjin, the current year also comprises expenses associated with the harmonisation of existing pension schemes. The ratio of expenses to revenue decreased to 13.3 % (previous year: 13.8 %).

Depreciation and amortisation rose slightly by 0.1 % year-on-year to € 122.6 million (previous year: € 122.4 million).

Against the background of these developments, the operating result before depreciation and amortisation (EBITDA) rose by 3.3 % to € 295.8 million (previous year: € 286.4 million) and thus more slowly than revenue. There was a corresponding moderate decrease in the EBITDA margin to 23.6 % (previous year: 24.3 %).

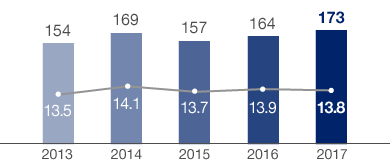

Operating Result (EBIT)

in € million/EBIT margin in %

The operating result (EBIT) increased by 5.6 % to € 173.2 million in the reporting period (previous year: € 164.0 million). As this rise was broadly in line with revenue, the EBIT margin remained virtually unchanged at 13.8 % (previous year: 13.9 %). In the Port Logistics subgroup, EBIT rose by 6.1 % to € 156.6 million (previous year: € 147.6 million). As a result, the subgroup accounted for 90.4 % (previous year: 90.0 %) of the Group’s operating result in the reporting period. In the Real Estate subgroup, EBIT grew by 1.5 % to € 16.3 million (previous year: € 16.0 million). 9.6 % of the Group’s operating result was generated by this subgroup (previous year: 10.0 %).

Net expenses from the financial result increased by € 7.9 million or 44.0 % to € 25.9 million (previous year: € 18.0 million). This was mainly due to the revaluation of an equalisation liability payable to a minority shareholder in conjunction with a profit and loss transfer agreement. Positive exchange rate effects from the appreciation of the Czech currency and a reduction in expenses due to trends in the Ukrainian currency had an opposing effect.

At 28.1 %, the Group’s effective tax rate was on a par with the previous year.

Profit after tax and minority interests increased by 11.0 % year-on-year to € 81.1 million (previous year: € 73.0 million). Non-controlling interests accounted for € 24.8 million in the 2017 financial year (previous year: € 32.0 million). From a financial point of view, this item includes the expenses mentioned in relation to the financial result associated with revaluing the settlement obligation to a minority shareholder. Earnings per share rose by 11.0 % to € 1.11 (previous year: € 1.00). The listed Port Logistics subgroup achieved an 11.7 % increase in earnings per share to € 1.02 (previous year: € 0.91). Earnings per share of the non-listed Real Estate subgroup were up on the prior-year figure at € 3.65 (previous year: € 3.44). As in the previous year, there was no difference between basic and diluted earnings per share in 2017. The return on capital employed (ROCE) was up 0.7 percentage points year-on-year at 13.1 % (previous year: 12.4 %). see also Corporate and Value Management

As in the previous year, HHLA’s appropriation of profits is oriented towards the development of the HHLA Group’s earnings in the financial year ended. The distributable profit and HHLA’s stable financial position form the foundation of the company’s consistent profit distribution policy. On this basis, the Executive Board and Supervisory Board will propose at the Annual General Meeting on 12 June 2018 a dividend distribution of € 0.67 per Class A share and € 2.00 per Class S share. Based on the number of shares with dividend entitlement as of 31 December 2017, the sum distributed for listed Class A shares would increase by 13.6 % to € 46.9 million (previous year: € 41.3 million). At € 5.4 million, the amount paid out for non-listed Class S shares would be unchanged from the previous year. In relation to the consolidated profit and earnings per share, the dividend payout ratio would reach a high figure of approximately 66 % for the Port Logistics subgroup (previous year: 65 %) and around 55 % for the Real Estate subgroup (previous year: 58 %).

A TEU is a 20-foot standard container, used as a unit for measuring container volumes. A 20-foot standard container is 6.06 metres long, 2.44 metres wide and 2.59 metres high.

Vessels which carry smaller numbers of containers to ports. From Hamburg, feeders are primarily used to transport boxes to the Baltic region.

A TEU is a 20-foot standard container, used as a unit for measuring container volumes. A 20-foot standard container is 6.06 metres long, 2.44 metres wide and 2.59 metres high.

Transportation via several modes of transport (water, rail, road) combining the specific advantages of the respective carriers.

Revenue from sales or lettings and from services rendered, less sales deductions and VAT.

Revenue from sales or lettings and from services rendered, less sales deductions and VAT.

In maritime logistics, a terminal is a facility where freight transported by various modes of transport is handled.

Transportation via several modes of transport (water, rail, road) combining the specific advantages of the respective carriers.

Earnings before interest, taxes, depreciation and amortisation.

Earnings before interest and taxes.

Earnings before interest and taxes.

Interest income – interest expenses +/– earnings from companies accounted for using the equity method +/– other financial result.

EBIT / Average Operating Assets.